Federal Student Loan Repayment Changes

As we gear up for July 4th celebrations, sweeping changes to the federal student loan program threaten to soak up some of the spotlight. This article serves as a framework for working through debt repayment options for existing and new student loan borrowers.

Student Loan Repayment Programs:

There are currently two types of debt repayment plans for federal student loans: Income-Driven & Standard Repayment.

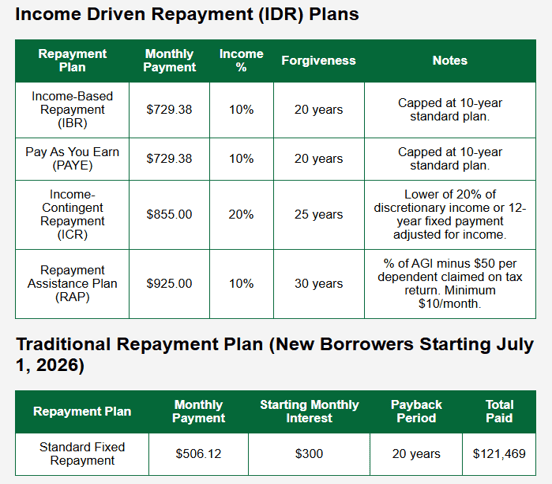

Income-Driven Repayment Plans (IDR) - Monthly payments are defined by a portion of discretionary income that factors in a person’s Adjusted Gross income, family size, and protective income guardrails. In other words, a portion of a borrower’s income is used to determine a monthly payment amount after accounting for their basic living expenses. These amounts are subject to change after an annual income recertification.

Current IDR options are Income-Based Repayment (IBR), Income-Contingent Repayment (ICR), and Pay As You Earn (PAYE). These plans qualify for Public Student Loan Forgiveness (PSLF) and long-term forgiveness. The Savings on a Valuable Education (SAVE) plan was previously an option but dismantled in March 2026.

Standard Repayment Plans - Fixed monthly payments are determined by the initial loan balance, interest rate, and term of the loan. The standard is a 10-year plan.

On July 1, 2026, borrowers with existing loans in certain IDR plans will have a decision to make.

- IBR Plan (Old & New) – Plans will remain intact, no action needed.

- PAYE & ICR Plans – Both of these plans will be phased out on July 1, 2028. Loans in these plans will be transitioned to IBR or Repayment Assistance Plan (RAP), described below, if no action is taken by then.

- SAVE Plan - This plan no longer exists. Loan servicers will give borrowers 90 days to move their existing loans to an IBR or RAP plan.

Note: If borrowers in PAYE or ICR plans are estimated to reach forgiveness before July 1, 2028, it will likely be prudent to stay put in most cases.

Post-July 1, there will be only two repayment options available for new loans:

- Repayment Assistance Plan (RAP) - This new Income-Driven plan omits the discretionary income factor and mainly uses a portion of a borrower’s Adjusted Income (AGI) for monthly payment calculations. RAP loans will have longer terms than legacy IDR plans and incorporate a sliding scale that increases monthly payments as AGI increases. Scale: 1% - 10% of AGI

- Tiered Standard Plan - Fixed monthly payments are computed like the old standard plan but initial loan balances now determine the repayment terms. The larger the balance, the longer the repayment period. Terms: 10, 15, 20, and 25 years

Below is a comparison assuming an existing IBR loan for $80,000 with a 4.5% interest rate. The borrower is a Single household with an AGI of $111,000:

Source: EDCAP's Repayment Plan Calculator - EDCAPNY.org

When we put numbers behind these formulas, the differences can be stark.

IBR vs. RAP: In this example, monthly payments are $196 more under RAP, and this borrower would assume 10 additional years of payments in theory. One thing to note is that this borrower is already at the highest band on the AGI scale for RAP (10%).

The RAP plan has no caps on monthly payments. From a financing angle, increasing payments over time will likely wipe out balances before the 30-year mark but placing no limits on increasing required monthly payments may likely strain family budgets.

This RAP calculator provides specific information on a borrower’s situation.

IBR vs. Standard: At first glance it may appear that the Standard Repayment offers the “best” deal, but that picture may change with some added context.

Example: If this borrower is a sales professional that mainly relies on commissions, here is how monthly payments in an IBR plan would shake out with an initial $80,000 balance:

Bad Year

AGI: $70,000 | $387.71

Average Year

AGI: $100,000 | $637.71

Great Year

AGI: $300,000 | $829.11

Payment cap: While the $506.12 remains fixed for 20 years on the Standard plan, IBR payments adjust annually and will never exceed the 10-year standard amount. In this context, $829.11 is the predetermined max IBR payment based on the initial loan terms.

In fairness, monthly payments under RAP would also adjust downward with a reduction in AGI. Monthly payments would be $350 and $750 respectively for the bad and average sales years. The cap truly shines with an upward trajectory in income. In the Great Year, the borrower would be subject to a $2,500 monthly payment for the year under RAP vs $829.11 for the IBR plan.

Note: The ability to pay less than the 10-year standard amount under the IBR, ICR, and PAYE plans at points can lead to growing outstanding balances over time.

If a fixed payment amount works for a borrower’s budget, then the Standard plan is the most economical way to pay down their debt.

The main takeaway for borrowers is to opt into an affordable repayment plan, so they can have the flexibility to tackle their outstanding balances as they see fit.

Evaluating Options:

Before crunching all the numbers, how can borrowers with existing or post-July 1 federal student loans think through their repayment options?

Case for the Tiered Standard Plan:

- Simple and favorable repayment structure: fixed payments, competitive interest rate, and term limit.

- Stable income sources.

- No consideration for Public Student Loan Forgiveness (PSLF) and long-term forgiveness.

- Federal Protections: Payment deferment or forbearance.

This plan suits borrowers that have manageable balances compared to their stable income sources, seek simplicity, and value the ability to apply for deferment or forbearance during tough times.

Case for the IBR Plans (Eligible pre-July 1 loans):

- Similar structure to IDR plans that have or will phase out: SAVE, ICR, and PAYE.

- Eligible for PSLF and long-term forgiveness.

- High income earners with modest or big loan balances.

- Federal Protections: Monthly payments can be adjusted to $0 in extreme cases.

For borrowers with loans in SAVE, PAYE, and ICR plans, the eventual switch to the old or new IBR plan will likely be the closest thing to a seamless transition due to the similarities in the repayment structures and established family budgets.

Case for the RAP Plan:

- Lower-income borrowers with modest or big balances.

- Only IDR option for PSLF and long-term forgiveness for post-July 1 loans.

- Bridge repayment structure for future high earners and certain professionals in transition.

- Federal Protections: Interest Subsidy and Matching Principal Payment.

Note: Borrowers pursuing long-term forgiveness should consider the potential tax impacts on their forgiven balances. Amounts forgiven under eligible plans will be treated as taxable income. Public Service Loan Forgiveness (PSLF) remains tax-free.

The RAP plan can fall short during years of increasing income for high earners, but it truly shines for borrowers that need to prevent their loan balances from growing over time. The sliding scale feature also presents some planning opportunities.

Example: An aspiring doctor working to pay down their large student loan balance during residency could greatly benefit from the RAP interest subsidies in their lower earning years before opting for the Tiered Standard Plan or refinancing through private means when their practice takes off.

These changes brought forth by the One Big Beautiful Bill Act clean up the various repayment options of old, but some borrowers may be negatively impacted if proactive measures are not taken before certain deadlines.

As always, give us a call if you would like to discuss your student loan options!

Source:

OBBBA Breakout Guide: Key Student Loan Changes To Know